During a recession, the most effective investing strategies focus on

Maintaining a long-term perspective and continuing to invest systematically through dollar-cost averaging can help reduce risk and even create opportunity when markets recover.

What is a recession & how does it affect investments?

A recession is broadly defined as a significant decline in economic activity lasting more than a few months, typically visible in GDP, employment, income and consumer spending. The

During a recession, financial markets often experience:

- Falling stock prices as corporate earnings expectations decline

- Rising unemployment, which reduces consumer spending

- Increased

market volatility as investors react to uncertainty - Lower interest rates, as the Federal Reserve often cuts rates to stimulate growth

What this means for your portfolio: Recessions don't affect all investments equally. Some asset classes—like high-yield or "junk" bonds and speculative small-cap stocks—tend to be hit harder. Others—like investment-grade bonds, dividend-paying stocks and essential-service equities—historically hold up better.

Recessions are real, but they are temporary. Since World War II, the average U.S. recession has lasted approximately 10 months. The recoveries that follow are often longer and stronger.

Should you invest during a recession?

Yes, for most long-term investors, continuing to invest during a recession is generally the right approach. Here's why:

The case for staying invested:

- Pulling money out of the market locks in losses and risks missing the early stages of a recovery, which historically produce some of the strongest gains

- Recessions can create buying opportunities, as quality assets are often available at lower prices

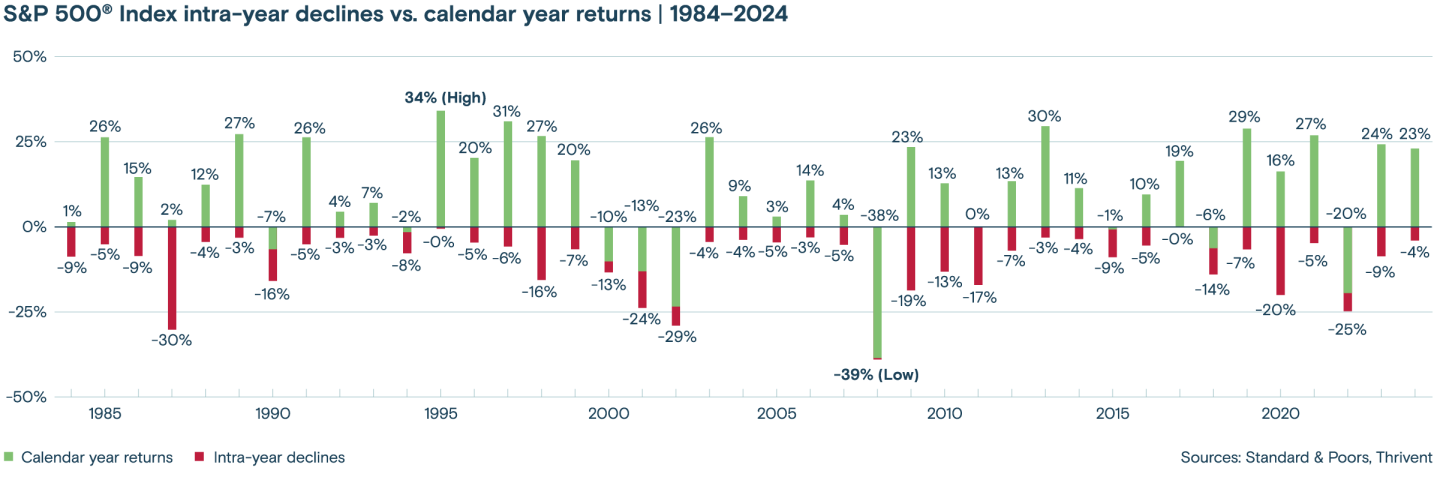

- Over the last 40+ years, the S&P 500 has ended the calendar year in positive territory more than 75% of the time—despite often experiencing significant intra-year drops

The case for adjusting your strategy:

- If your time horizon is short (e.g., you're retiring in 1–3 years), reducing exposure to high-volatility assets makes sense

- If your emergency fund isn't sufficient (typically 3–6 months of expenses), shoring up cash reserves before investing more is prudent

The bottom line: Don't stop investing, but do invest thoughtfully. A

The economic cycle & where recessions fits

The economy moves in cycles, and each phase carries different investment implications. Understanding where you are in the cycle helps you make more intentional decisions rather than reactive ones.

The economic cycle

No two economic cycles are identical, and transitions between phases aren't always predictable. That's why diversification—rather than attempting to perfectly time each phase—remains the most reliable long-term approach.

The importance of diversification

Diversification is the practice of spreading investments across different

When you hold a mix of stocks, bonds, real estate and cash equivalents, some assets may decline while others hold steady or even

A diversified portfolio typically includes:

- Equities (domestic and international, large- and small-cap)

- Fixed income (government and investment-grade corporate bonds)

- Real assets (REITs, commodities)

- Cash and cash equivalents (money market funds, CDs, high-yield savings)

To keep diversification working as intended, you should review and

Remember, diversification can reduce risk, but it does not eliminate it. It does not guarantee a profit or fully protect against losses in a declining market.

Don't forget dollar-cost averaging

Go deeper:

Suppose you invest $500 per month into an index fund. When prices are high, your $500 buys fewer shares. When prices drop during a recession, that same $500 buys more shares at a lower cost. Over time, this can reduce your average cost per share and position you well for recovery.

Benefits of DCA during a recession:

- Removes the pressure and guesswork of timing the market

- Transforms market dips into buying opportunities

- Builds consistent investing habits that support long-term wealth

Important note: Dollar-cost averaging does not guarantee a profit or protect against losses. But it does reduce the risk of making large lump-sum investments at market peaks—a particularly valuable feature during uncertain times. If you contribute regularly to a 401(k) or IRA, you're likely already practicing dollar-cost averaging.

7 common recession investments

The best recession investments tend to share some common traits: they're tied to essential goods or services, they generate income, or they've historically shown lower sensitivity to economic downturns. Here's a breakdown of the main options:

1. Large-cap stocks

Large-cap companies—typically those with

That said, not all large-cap

2. Dividend-paying stocks

Stocks that pay consistent

Reinvesting dividends during a downturn can also meaningfully accelerate recovery and long-term growth.

3. Investment-grade bonds

Bonds are a cornerstone of recession-resilient portfolios. Here's why:

- Inverse relationship with interest rates: When the Federal Reserve cuts rates to stimulate the economy during a recession, existing bond prices typically rise.

- Predictable income: Bonds pay a fixed interest rate (coupon) over a set term, providing reliable cash flow.

- Capital preservation: Higher-quality bonds, particularly U.S. Treasuries and investment-grade corporates, historically preserve capital better than equities during downturns.

Bond types to consider during a recession:

- U.S. Treasury bonds: Backed by the federal government; considered one of the safest investments available

- Investment-grade corporate bonds: Issued by financially stable companies with strong credit ratings

- I Bonds: Government-issued savings bonds that adjust for inflation; useful if inflation remains elevated alongside a recession

Avoid: High-yield (junk) bonds during recessions. These are issued by companies with lower credit ratings and carry significantly higher default risk when the economy contracts.

4. ETFs & mutual funds

Types of funds worth exploring during downturns:

- Bond ETFs focused on Treasuries or investment-grade corporates

- Dividend ETFs targeting companies with strong payout histories

- Balanced/

asset allocation funds that automatically maintain a diversified mix across stocks and bonds

Thrivent’s

5. Real estate & REITs

REITs (Real Estate Investment Trusts) allow you to invest in real estate without owning physical property. They're required by law to distribute at least 90% of taxable income to shareholders as dividends, making them attractive income generators. Certain REIT sectors—such as residential, healthcare and self-storage—tend to be more recession-resilient because demand remains relatively steady regardless of the economic cycle.

6. Commodities & precious metals

Commodities like

Caution: Industrial metals (copper, aluminum) are tied to manufacturing activity and may decline during recessions as production slows. Be selective.

7. Cash and cash-equivalents

Cash-equivalent options to consider:

High-yield savings accounts : FDIC-insured, liquid and currently offering competitive interest rates above traditional savings accountsCertificates of deposit (CDs) : Fixed-term deposits with guaranteed interest rates, insured up to $250,000 per depositor by the FDIC. CD laddering (staggering maturity dates) can help balance liquidity and yieldMoney market funds : Low-risk mutual funds that invest in short-term, high-quality securities; offer modest returns with daily liquidity. Note: Unlike bank accounts, money market funds are not FDIC-insured, though they aim to maintain a stable $1.00 per share valueTreasury bills (T-bills) : Short-term U.S. government securities (four-week to 52-week terms) that are considered among the safest assets available and are exempt from state and local taxes

Before investing more aggressively, most financial planners recommend having three to six months of living expenses in accessible, low-risk accounts.

Investing by life stage: How recession strategy shifts with age

Recession investment strategy should be tailored to your time horizon and financial situation. Here's a general framework.

In your 20s and 30s (long horizon)

- You can generally afford to stay invested in equities and ride out downturns.

- Continue contributing to 401(k) and IRA accounts—you're buying at lower prices.

- For 2026, the IRS contribution limit for a 401(k) is $24,500 ($32,500 if age 50+); the IRA limit is $7,500 ($8,600 if age 50+, reflecting the new

SECURE 2.0 cost-of-living adjustment to the catch-up contribution). - Focus on building your

emergency fund alongside investing.

In your 40s and 50s (mid-range horizon)

- Gradually shift toward a more balanced allocation (e.g., 60% stocks / 40% bonds).

- Review your target date fund settings if applicable.

- Avoid making dramatic portfolio changes based on short-term market moves.

Near or in retirement (short horizon)

- Protecting capital becomes a higher priority; consider increasing your allocation to bonds, dividend stocks and cash equivalents.

- Review your withdrawal strategy; avoid selling equities at depressed prices to fund living expenses if possible.

- A bucket strategy (segmenting money by time horizon) can help provide stability.

Historical market performance: Why staying invested matters

Over the past four decades, the U.S. stock market has demonstrated remarkable long-term resilience. The S&P 500 has closed the calendar year in positive territory more than 75% of the time—even accounting for years that experienced significant intra-year drops.

This doesn't mean recessions don't hurt. They do. But historically, the pain has been temporary, while the recovery has been durable. Economic downturns can rattle even seasoned investors, but they always have passed. Keep the bigger picture in mind as you take steps to build, balance and diversify your portfolio.

Recession investing FAQ

Is it better to hold cash or invest during a recession?

What happens to my 401(k) during a recession?

Are bonds safe during a recession?

How long do recessions typically last?

Should I rebalance my portfolio during a recession?

What are the best sectors to invest in during a recession?

Get the investing guidance you need

When there are signs of a downturn on the way—and even when there aren't—you always can connect with a